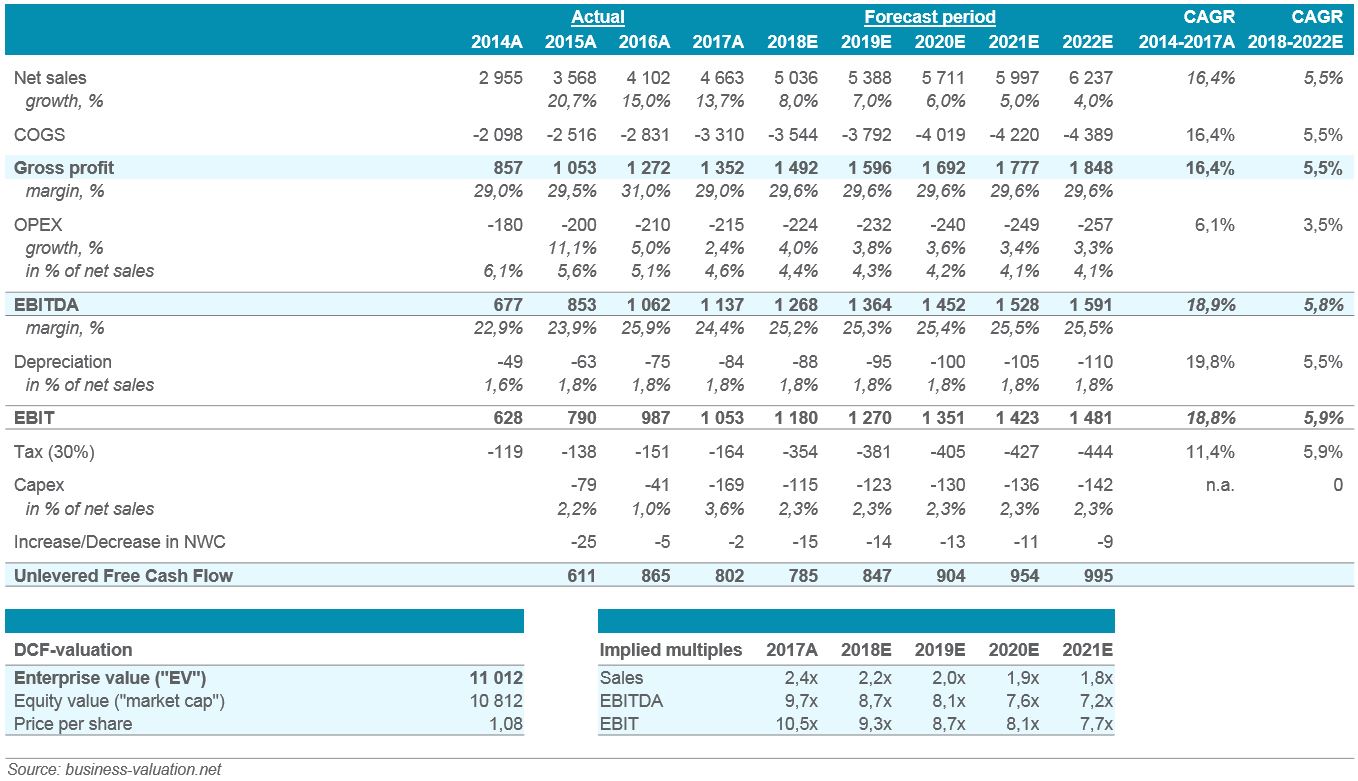

Discounted cash flow valuation

Definition of Discounted cash flow valuation

The Discounted cash flow valuation is the most generally accepted and performed as of today, often referred to as the DCF model. The value of a company is obtained by a forecast of a company’s accumulated future cash flows discounted to the present at the weighted average cost of capital (WACC).

The Discounted cash flow valuation (DCF)

The DCF valuation is based on the idea that a company’s value is driven by its ability to generate cash flow over the long term in the future and in addition, the company’s cash flow generating ability is driven by its long-term growth and its returns above its cost of capital. Using the long-term growth and the returns above its cost of capital helps to understand of the value creation at a company.

The formula for calculating net present value (NPV) for infinitive time period will be expressed as:

NPV = CF0 + CF1/(1+ r) + CF2/(1+ r)2 + CF3/(1+ r)3 + …

Alternatively for limited time period due to M&A or sale of the company

NPV = CF0 + CF1/(1+ r) + CF2/(1+ r)2 + CF3/(1+ r)3 + … CFt/(1+ r)t + Tt/(1+ r)t

Where CFt = cash flow at time t, T = terminal value at t and r = WACC

T = CFt/(r – g)

Where g = growth rate of the cash flow

Under assumption of stable growth

WACC = Ke [E/(E + D)] + Kd (1 – t)[D/(E + D)] Where Ke = cost of equity, Kd = cost of debt and t = corporate tax rate

Ke = Rf + β(Rm – Rf)

Where Rf = risk-free rate, Rm = expected market return, β = equity beta

The calculation from revenues to cash flow will be expressed using valuables from a company’s income statement as:

– Cost of goods (excl. depreciation)

– Depreciation expense

Earnings before interest and taxes (EBIT)

– Cash taxes on EBIT

Net operating profit less adjusted taxes (NOPLAT)

+ Depreciation

Gross cash flow

– Increase in operating working capital

– Investments

Cash flow (CF)

DCF model

One of the main advantages of the DCF valuation model is that the variables of the valuation model are flexible for changes in a company’s environment. But this is also one of the main disadvantages, since the valuation model consists of a diverse set of variables that are based on assumptions of the future and therefore, even the most detailed and careful valuation cannot provide a precise estimate of value. Assumptions have to be made concerning the future of the company and the economy in general. All these assumptions are also colored by the bias of the analyst who is performing the valuation.

Given this reason, large companies with table revenues and well-known markets will naturally be possible to value with greater precision than smaller and/or younger companies involved in new technologies or projects with uncertain future. Other models worth to point out in this context is the economic profit model, the equity discounted cash flow model, which is best suited for financial institutions such as banks and insurance companies, and the adjusted present value (APV) model, which is best suited for companies with changing capital structures. Performed correctly all of these should give about the same results.

Recent Comments